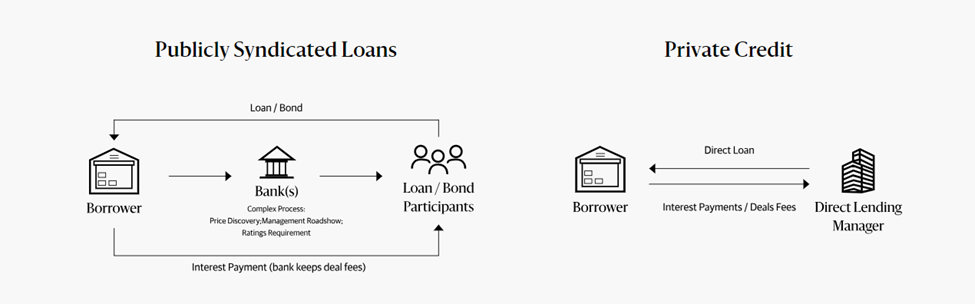

Beyond the world of public stocks and bonds lies a vast, multi-trillion dollar universe of private credit and real-world assets (RWAs). This includes everything from corporate loans, trade receivables, infrastructure debt, and equipment leases. These assets form the backbone of the real economy and offer attractive, stable yields.

However, for most institutions, this market has been notoriously difficult to access. Investing in private credit today is a slow, opaque, and paper-intensive process. Once you’ve invested, your capital is effectively locked up; there is almost no secondary market to trade these assets.

This illiquidity creates a massive drag on the market’s potential. VOLS is engineered to solve this, providing the market infrastructure to transform these static, real-world assets into programmable, liquid, and transparent digital instruments.

What is Private Credit securitisation?

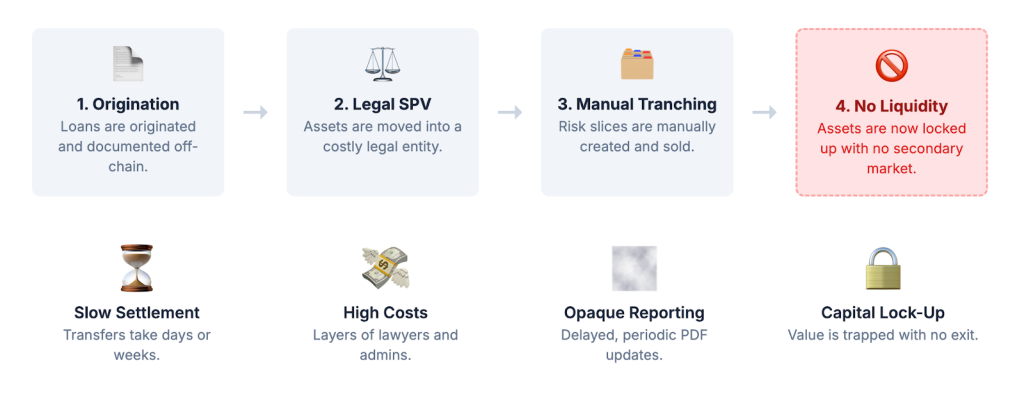

At its core, securitisation is the process of taking illiquid assets—like a bundle of small business loans, packaging them together, and selling slices of that package to investors. Each slice, or “tranche,” carries a different level of risk and potential return. This allows lenders to get loans off their books to free up capital, and it gives investors access to different types of credit assets. While powerful in theory, the traditional way of doing this is incredibly inefficient.

The current process for creating and selling these credit products is a tangled web of lawyers, administrators, and disconnected systems that add significant time and cost.

The Traditional Workflow in Action:

- A fintech company originates a batch of loans to small businesses.

- These loans are legally sold to a Special Purpose Vehicle (SPV), a separate legal entity created solely to hold the assets. This is a paper-heavy, costly legal process.

- The SPV issues notes to investors in different risk tranches (e.g., senior, junior).

- An administrator manually manages loan repayments, handles defaults, and sends out periodic PDF reports to investors, often only monthly or quarterly. Investors have limited real-time visibility into the performance of their assets.

- Selling a slice of this package is nearly impossible. Ownership transfers are slow, taking days or weeks, and require intermediaries. There is effectively no secondary liquidity.

This workflow is defined by its opacity, high costs, and profound illiquidity, which keeps trillions of dollars in value locked up and inaccessible.

A New, Transparent Workflow

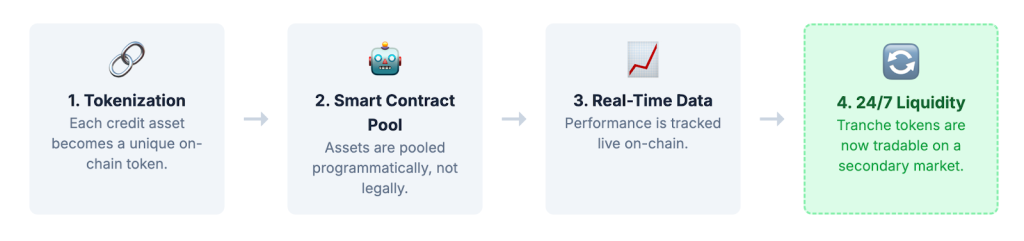

By representing each loan or credit asset as a unique digital token on a blockchain, we can collapse the entire cumbersome workflow into a single, transparent, and automated process.

The DeFi-Powered Workflow:

- Tokenization: Each loan agreement is represented as a digital token. Its data and performance history are digitally native and verifiable in real time.

- On-Chain Pooling: Instead of a complex legal SPV, a smart contract acts as a transparent, automated vehicle. It programmatically bundles the loan tokens into a digital pool, with all its rules and cash flows auditable on-chain.

- Automated Tranching: The smart contract automatically creates digital tokens representing the different risk tranches

- Real-Time Reporting: As borrowers make payments, the smart contract automatically streams the principal and interest to the wallets of the tranche token holders. Investors can watch their assets perform in real-time on a dashboard; no more waiting for delayed PDF statements.

- Instant Secondary Liquidity: This is the game-changer. An investor can sell their “Senior_Tranche_Token” on a 24/7 marketplace like VOLS at any time, turning a previously illiquid asset into a liquid one.

VOLS: The Institutional-Grade Infrastructure for On-Chain Credit

This new on-chain credit market requires purpose-built infrastructure to function at an institutional level. VOLS provides the three critical layers to make this a reality:

- The Marketplace: VOLS provides an institutional-grade Central Limit Order Book where these newly liquid credit tranche tokens can be traded. This creates a vibrant secondary market, enabling real-time price discovery and allowing institutions to dynamically manage their credit portfolios for the first time.

- The Insurance Layer (iAssets): VOLS’s integrated insurance layer allows institutions to actively manage risk. Insurance vaults can underwrite the default risk of loan pools, and this credit protection is tokenized as an “iAsset”. This creates a new, on-chain equivalent to credit default swaps, allowing for sophisticated hedging and risk transfer.

- The Compliance & Governance Core: VOLS is built for regulated adoption. Our platform ensures that all participants, from lenders to investors, are verified institutions through a Know-Your-Business (KYB) process, creating a compliant and secure environment for on-chain credit markets.

Putting It Into Practice:

An originator tokenizes $50M in SME loans.

- A VOLS-compatible smart contract issues two tranches: a low-risk Senior tranche and a high-risk Junior tranche.

- Both tranche tokens are listed for trading on the VOLS CLOB.

- A VOLS insurance vault underwrites the default risk of the Senior tranche, issuing a tradable iAsset as protection.

- Institutional investors can now buy, sell, and hedge these credit assets in real-time on a single, integrated platform.

The Strategic Imperative

Tokenizing real-world assets is one of the single largest opportunities in modern finance. By providing the essential infrastructure for secondary liquidity, on-chain risk management, and regulatory compliance, VOLS is positioned to become the central clearinghouse for this new, on-chain private credit ecosystem. This will unlock unprecedented access and efficiency for institutions, channeling capital to the real economy more effectively than ever before.

VOLS offers institutions a unique opportunity: the ability to access on-chain yield, execution, and governance, without surrendering control, transparency, or risk management.

It’s the first DeFi-native infrastructure to bring together:

- The execution discipline of a regulated exchange

- The flexibility of programmable liquidity strategies

- The safety of native insurance and governance